What is Real Estate Mortgage Investment Conduit (REMIC)?

Learn what a Real Estate Mortgage Investment Conduit (REMIC) is, how it works, and its benefits for investors and the mortgage market.

Introduction to Real Estate Mortgage Investment Conduits (REMICs)

If you’re exploring mortgage-backed securities, you’ve likely come across the term Real Estate Mortgage Investment Conduit, or REMIC. Understanding REMICs can help you grasp how mortgage pools are structured and traded in the financial markets.

In this article, we’ll break down what a REMIC is, how it functions, and why it matters to investors and the mortgage industry. You’ll get clear insights into this important financial vehicle.

What is a REMIC?

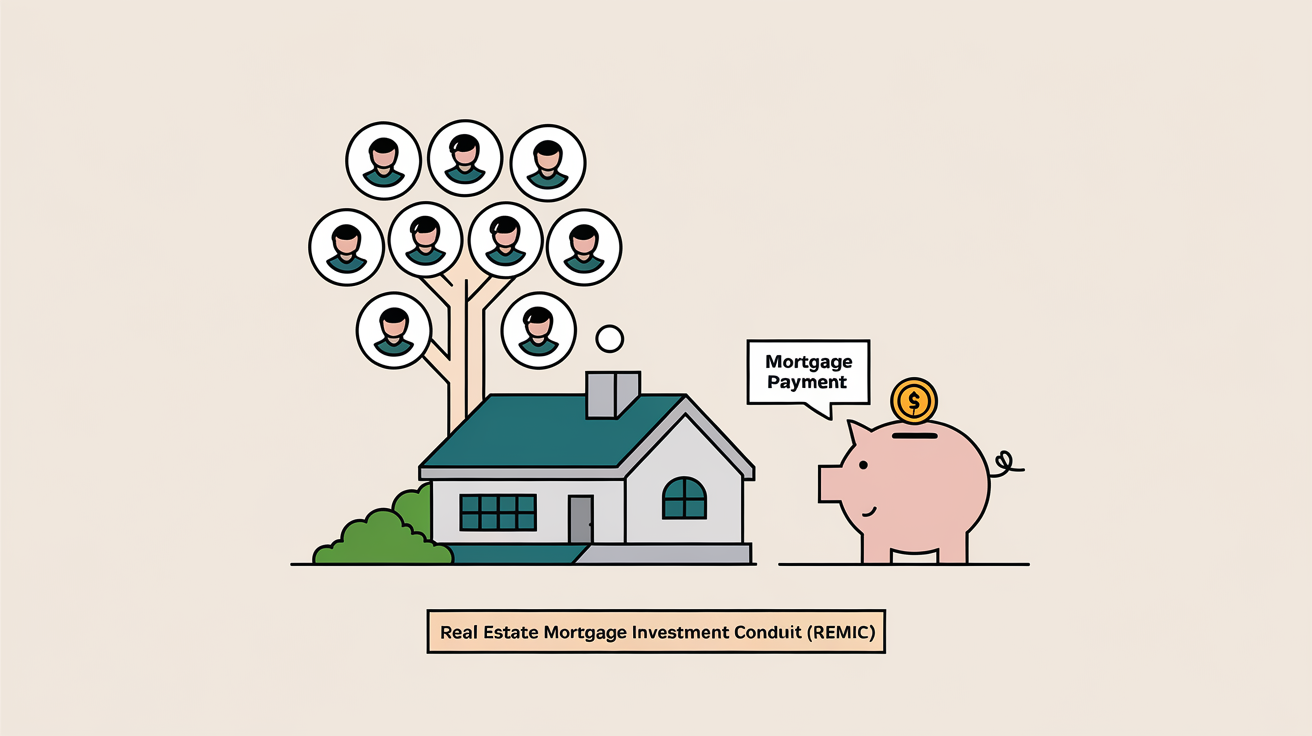

A Real Estate Mortgage Investment Conduit (REMIC) is a special purpose vehicle created to hold a pool of mortgages and issue mortgage-backed securities (MBS) to investors. REMICs were introduced by the U.S. Tax Reform Act of 1986 to provide a tax-efficient way to package and sell mortgage loans.

REMICs allow mortgage pools to be divided into different classes or tranches, each with distinct risk and return profiles. This structure helps investors choose securities that match their investment goals.

Key Features of REMICs

- Pass-through taxation:

REMICs are not taxed at the entity level, avoiding double taxation.

- Multiple classes:

They can issue various classes of securities with different maturities and payment priorities.

- Mortgage pools:

REMICs hold residential or commercial mortgage loans or mortgage-backed securities.

- Regulated structure:

They must meet specific IRS rules to qualify for REMIC status.

How Does a REMIC Work?

REMICs start by acquiring a pool of mortgages or mortgage-backed securities. These assets generate cash flows from borrowers’ principal and interest payments. The REMIC then issues securities backed by these cash flows.

Investors buy these securities, which are structured into different classes, such as:

- Regular interests:

These receive principal and interest payments.

- Residual interests:

These receive remaining cash flows after regular interests are paid.

This division allows investors to select securities based on risk tolerance and expected returns.

Benefits of REMIC Structure

- Tax efficiency:

REMICs avoid entity-level taxation, passing income directly to investors.

- Flexibility:

They can structure securities with varying maturities and risk levels.

- Liquidity:

REMIC securities are often traded in secondary markets, providing liquidity to investors.

- Transparency:

REMICs must comply with strict IRS rules, ensuring clear reporting and disclosure.

REMICs in the Mortgage Market

REMICs play a vital role in the U.S. mortgage market by enabling lenders to package loans and sell them to investors. This process frees up capital for lenders to issue more mortgages.

Government-sponsored enterprises like Fannie Mae and Freddie Mac often use REMIC structures to issue mortgage-backed securities. This supports the housing market and promotes homeownership.

Types of Mortgages in REMICs

- Residential mortgages:

Single-family home loans are the most common.

- Commercial mortgages:

Loans on commercial properties can also be pooled.

- Hybrid pools:

Some REMICs combine different types of mortgage assets.

Risks Associated with REMIC Investments

While REMICs offer benefits, investors should be aware of risks such as:

- Prepayment risk:

Borrowers may repay loans early, affecting cash flows.

- Credit risk:

Defaults on underlying mortgages can reduce payments.

- Interest rate risk:

Changes in rates can impact the value of REMIC securities.

Understanding these risks helps investors make informed decisions about REMIC-backed securities.

Conclusion

Real Estate Mortgage Investment Conduits (REMICs) are important financial structures that package mortgage loans into tradable securities. They provide tax advantages, flexibility, and liquidity to investors in the mortgage market.

By understanding how REMICs work and their role in the housing finance system, you can better evaluate mortgage-backed securities as part of your investment strategy.

FAQs about REMICs

What types of mortgages can a REMIC hold?

REMICs can hold residential mortgages, commercial mortgages, or mortgage-backed securities, depending on the pool’s structure.

How do REMICs avoid double taxation?

REMICs are treated as pass-through entities for tax purposes, so income is taxed only at the investor level, not at the REMIC level.

Who typically issues REMIC securities?

Government-sponsored enterprises like Fannie Mae and Freddie Mac commonly issue REMIC securities, along with private financial institutions.

What is prepayment risk in REMICs?

Prepayment risk occurs when borrowers pay off mortgages early, which can reduce expected interest income for investors.

Are REMIC securities liquid investments?

Yes, many REMIC securities trade in secondary markets, offering liquidity to investors who want to buy or sell them.